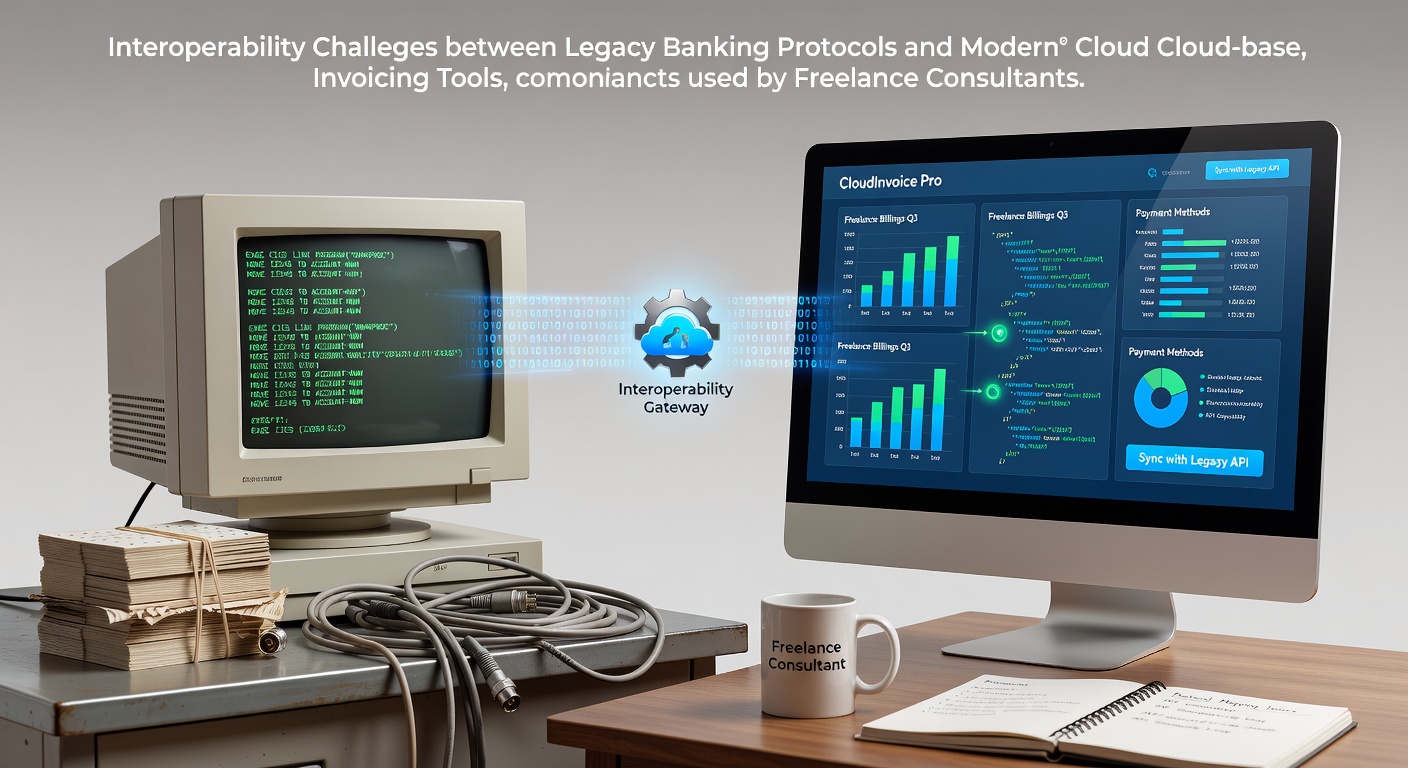

Exploring Interoperability Challenges Between Legacy Banking Protocols and Modern Cloud-Based Invoicing Tools Used by Freelance Consultants

Legacy banking protocols continue to shape financial data exchanges even as cloud-based invoicing platforms gain traction among freelance consultants, and these two worlds often collide over format mismatches, authentication barriers, and processing timelines that stretch across batch cycles rather than instant API calls. Observers note that many established banks still rely on protocols such as older ACH variants or SWIFT message structures designed decades ago, while tools like Xero or FreshBooks push real-time data flows through REST endpoints and webhooks.

Core Components of Legacy Banking Protocols

Protocols built around file-based transfers, including fixed-length records and batch submissions, handle reconciliation through overnight processing windows, and they require specific encryption layers plus dedicated network connections that predate modern web standards. Researchers from institutions across regions have documented how these systems prioritize stability over flexibility, which means consultants sending invoices from cloud dashboards encounter delays when banks demand exact header formats or manual approval steps before funds move. Data shows that compliance requirements tied to older rules around transaction reporting add further layers of validation that cloud platforms must replicate manually or through custom middleware.

Modern Cloud Invoicing Platforms in Practice

Cloud services designed for independent professionals automate invoice generation, tax calculations, and client reminders through intuitive dashboards that connect directly to accounting ledgers, yet they depend on open APIs and OAuth flows that legacy banks frequently do not expose. Those who manage freelance workflows report that integration attempts often stall at the point where a platform tries to push payment status updates back into a bank's proprietary file system. Figures from industry analyses reveal rising adoption rates among consultants who handle cross-border clients, which amplifies the friction when currency fields or reference numbers fail to map cleanly between systems.

Key Interoperability Barriers Identified

Format incompatibility ranks high among documented hurdles because legacy protocols expect rigid structures while cloud tools output JSON or XML variants that require transformation layers. Security handshakes present another layer since older systems favor certificate-based or VPN tunnels instead of token exchanges common in cloud environments. And processing windows create timing gaps because batch settlements in banking contrast with the on-demand nature of invoicing updates, leading to mismatched records that consultants must reconcile by hand. In June 2026 several regulatory updates from bodies in Canada and the EU highlighted the need for standardized bridging mechanisms, yet implementation remains uneven across institutions.

Take one consultant managing European clients who discovered that an automated payment confirmation from a cloud tool arrived in a format the receiving bank could not parse without manual intervention, forcing repeated resubmissions. Similar patterns appear in reports tracking small-scale operations where time spent on workarounds reduces billable hours. Evidence suggests authentication mismatches compound these issues when multi-factor requirements on banking sides conflict with session tokens used by cloud providers.

Regional Approaches and Emerging Standards

Authorities in Australia have examined open banking frameworks that encourage API exposure from traditional institutions, whereas counterparts in the United States focus on incremental updates to existing settlement rails. Academic studies from varied universities point to middleware solutions that translate between protocol generations, although these add operational costs and potential points of failure. What's interesting is how some banks have begun piloting hybrid gateways that accept both file uploads and limited API requests, creating pathways that reduce consultant friction without full system overhauls.

Consultants working across borders encounter additional variables around data residency rules and reporting obligations that differ by jurisdiction, and these rules sometimes dictate which protocol version a bank will accept. Research indicates that successful integrations often hinge on third-party connectors developed specifically for freelance use cases, yet availability varies by region and bank size.

Practical Examples from Consultant Workflows

One documented case involved a Canadian freelance analyst whose cloud invoicing tool generated recurring bills for international clients, yet the linked bank account processed confirmations only after daily batch cycles completed, resulting in delayed client notifications. Another instance tracked by industry observers showed a UK-based consultant adapting invoice templates to match legacy reference fields, which required custom scripting that the cloud provider later incorporated as an optional module. These examples illustrate recurring patterns where technical workarounds become part of routine operations.

Conclusion

Interoperability between legacy banking protocols and cloud invoicing tools remains an active area of development as institutions respond to demands from independent professionals, and progress depends on continued alignment of formats, security models, and processing schedules. Data from multiple regions shows gradual adoption of bridging technologies that ease data exchange without replacing core systems outright. Those tracking the space note that freelance consultants continue to navigate these gaps through a combination of manual checks and selective automation, with outcomes shaped by the specific banks and platforms involved.